- Release Date:2026-04-13

- Views:0

- Source:redoo

1. Market Overview

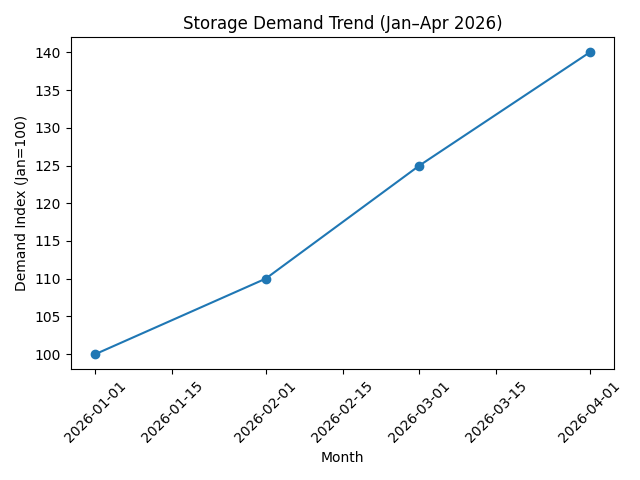

In April 2026, the global storage market — particularly DRAM and NAND Flash — continues to show a clear upward trend in both pricing and demand.

After a prolonged period of inventory correction throughout 2024, the market has now entered a new supply-tight cycle, driven by:

- Strong recovery in AI server deployments

- Continued expansion of cloud data centers

- Increasing demand from enterprise storage systems

- Gradual rebound in consumer electronics

As a result, both spot prices and contract prices have been rising steadily since Q1 2026.

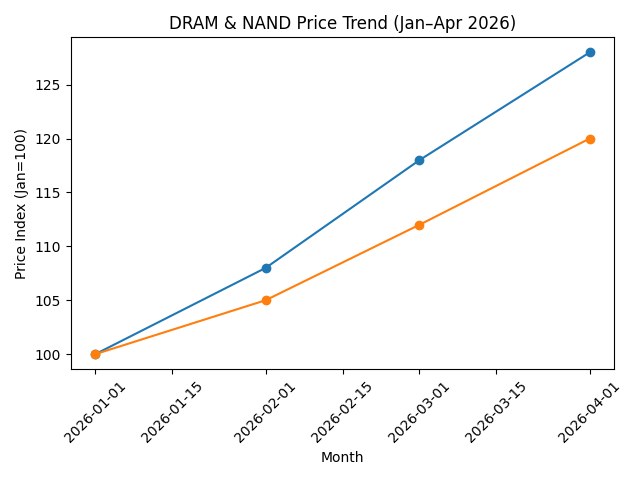

2. Price Trends: DRAM & NAND

📈 DRAM (DDR4 / DDR5):

- Prices increased approximately 10–20% in April

- DDR5 demand continues to outpace supply, especially in server applications

- Major suppliers are prioritizing high-margin AI and data center clients

📈 NAND Flash:

- Prices rose by 5–15%, depending on capacity and grade

- Enterprise SSD demand is significantly stronger than consumer SSD

- Suppliers are maintaining disciplined output control, preventing oversupply

👉 Key takeaway:

The market is shifting from buyer’s market → seller’s market

3. Demand Drivers

🔹 AI & Data Centers

- Large-scale deployments by cloud providers are consuming massive DRAM & SSD volumes

- AI training workloads require high bandwidth memory + high-capacity storage

🔹 Enterprise IT Infrastructure

- Ongoing upgrades in servers and storage arrays

- Increasing demand for high-reliability and long lifecycle components

🔹 Industrial & Embedded Systems

- Stable demand from automation, telecom, and edge computing

- Preference for long-term supply stability over lowest price

4. Supply Situation

Despite increased demand, supply remains constrained due to:

- Major manufacturers maintaining controlled production output

- Capacity allocation shifting toward advanced nodes (DDR5, high-layer NAND)

- Limited availability of certain legacy parts (DDR3 / lower-density NAND)

⚠️ This creates:

- Longer lead times

- Reduced spot availability

- Increased pricing volatility

5. What This Means for Buyers

For OEMs, ODMs, and procurement teams:

✅ Secure supply early — avoid last-minute sourcing

✅ Consider alternative brands or configurations

✅ Lock pricing where possible to avoid further increases

✅ Work with flexible suppliers who can access global channels

6. Outlook for May–June 2026

The upward trend is expected to continue in the near term:

- DRAM prices likely to rise further 5–10%

- NAND expected to remain stable or slightly increase

- Demand from AI infrastructure will remain the key driver

📌 Unless there is a sudden macroeconomic slowdown,

the storage market is expected to remain tight through Q2 2026